Capital Gains Tax was introduced to the South African Income Tax Act, 1962 (‘the Act’) from 1 October 2001 and is applicable to capital gains made after that date. The Act sets out the basis for taxing the capital gains arising from the disposal of an asset.

Capital Gains Tax (CGT) is payable on capital gains made within discretionary investments;

Model portfolios, just like other investment vehicles, may be subject to CGT;

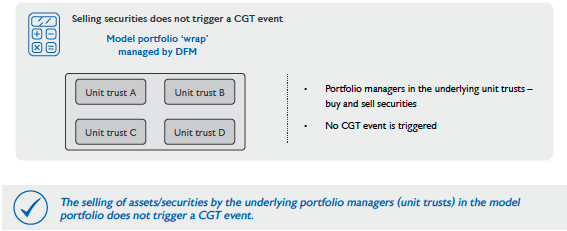

Selling assets/securities in the underlying unit trusts (funds) does not trigger a CGT event for model portfolios. However, a CGT event may be triggered when the discretionary fund manager (DFM) sells units;

The design of a model portfolio is key. It may lessen the CGT impact when selling (part of or all) your investments via asset allocation decisions and/or changes to the underlying mix of asset managers (unit trusts).

Capital Gains Tax was introduced to the South African Income Tax Act, 1962 (‘the Act’) from 1 October 2001 and is applicable to capital gains made after that date. The Act sets out the basis for taxing the capital gains arising from the disposal of an asset.

Key facts about CGT for investors

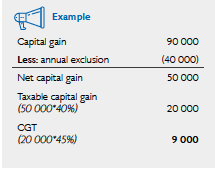

CGT is ONLY payable if the price of the investment (e.g unit trust) has risen since the date of investment. This increase in value is known as a capital gain and only becomes relevant when/if you decide to sell (part of or all) your investments. Thus, you decide when to become liable for CGT;

It is important to note that individual taxpayers enjoy an annual capital gain exclusion of R40 000. You therefore ONLY pay CGT on the amount above the R40 000 threshold;

Currently, ONLY 40% of the net capital gain and not the total gain, is included in your annual income, making the maximum CGT rate 18% for individuals paying the maximum 45% marginal tax rate.

Understanding the treatment of various types of capital gains is important. In this article, we aim to illustrate the impact of CGT when it comes to the type of investment vehicle/product you use, with a specific focus on model portfolios.

Dispelling the myth – ALL types of investments attract CGT

The selling of the underlying assets/securities held by the portfolio managers within the ‘underlying’ unit trusts (or funds), is not seen as a CGT event for either the unit trust company or investor.

The underlying portfolio managers are therefore able to focus on the core business of managing the portfolio according to their mandate, without having to concern themselves with tax issues.

Dispelling the myth – the need to rebalance a model portfolio’s asset allocation more frequently and/or replace one of the underlying unit trusts will result in additional CGT

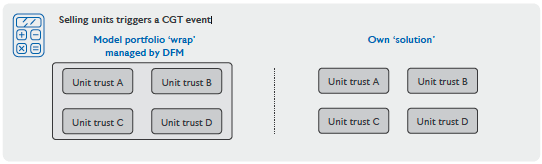

Firstly, it is not only model portfolios that attract CGT when rebalancing or when making changes to the mix of unit trusts. It is irrelevant whether you are invested in a DFM model portfolio or have constructed your own solution by combining a selection of unit trusts with or without the advice of a financial adviser. The rebalancing and/or replacement of any unit trust that requires the selling of units, MAY trigger a CGT event.

Secondly, the design of a model portfolio is important as it may reduce the CGT tax liability when applying a rebalancing policy. When a DFM uses multi-asset class portfolios with limited constraints and maximum flexibility (within regulations and reasonable concentration limits), it allows managers the maximum freedom to add value through asset allocation (strategic and tactical) and security selection across asset classes. The end result of multi-asset class (balanced) portfolios is that the DFM will need to make fewer changes to the asset allocation. This is in contrast to a specialist building block approach that may require more frequent rebalancing to align the portfolio to its strategic asset allocation.

Lastly, it is also an important discipline to make rational decisions when replacing a unit trust manager. 1Research from Allan Gray shows a weighted average fund holding period for investors – an individual fund churn rate – of just five years. It is therefore important to minimise manager changes. The less churn you incur, the less CGT you will be liable for. Limiting changes defers the CGT and lessens the risk of not achieving outcome expectations.

A DFM is expected to build long-term relationships with the underlying unit trust managers. The manner in which the managers have been combined in the model portfolio, should result in a low ‘churn rate’, as decisions made by the DFM are not based purely on past performance

In conclusion, we have tried to clarify a number of key issues relating to CGT in model portfolios. Most important to note is that irrespective of whether you are invested in a model portfolio or not, you cannot avoid CGT. All share portfolios, fund of funds and single unit trust (discretionary) investments may attract CGT on disposal of assets/units. But do not forget the annual R40 000 CGT exclusion – it will help reduce the pain.