The tax treatment of investment income – local vs foreign

Albert Louw

Head of Business Development

INVESTMENT INCOME = INTEREST AND DIVIDENDS

South African residents are subject to tax on their worldwide income. There is a difference in the way South African residents are taxed when investing locally or when investing abroad.

We provide a brief explanation of the tax treatment of local and foreign investment income/distributions for a tax resident individual in South Africa.

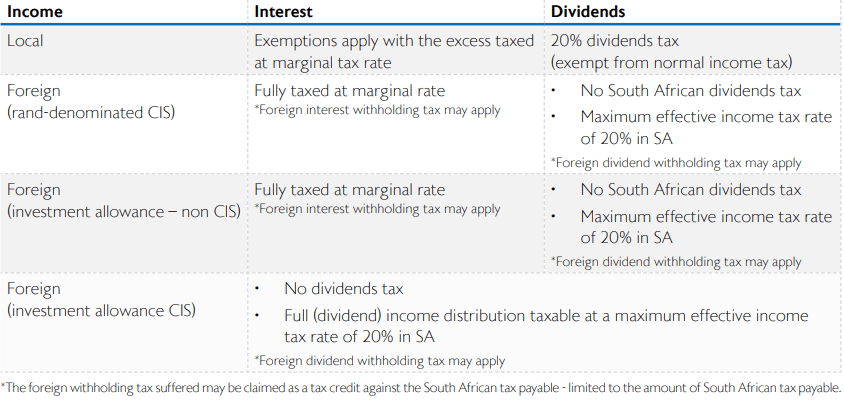

Summary table

Introduction

Each tax year, investors are issued with an IT3(b) certificate for local investment income and/or a statement for foreign investment income. This certificate/statement states the total interest and dividends earned locally and offshore during the course of the tax year. These amounts should then be included on tax returns submitted by the investor to SARS. Investors are entitled to claim a tax credit for any withholding tax paid in respect of a foreign dividend/interest that is included in gross income up to the amount of South African tax payable..

Interest

Local interest

Local interest is currently taxed (for the 2021 tax year) subject to the following exemptions:

- Under 65 years of age: R23 800

- 65 years of age and older: R34 500

The excess is taxed at the investor’s marginal tax rate, which varies between 18% and 45%..

Foreign interest

Foreign interest earned is fully taxable.

Dividends

Local dividends

A dividends tax of 20% is required to be withheld in respect of dividends received from South African resident companies and cash dividends from dual-listed companies. South African residents will receive the dividend less dividends tax of 20%.

As the dividend was subject to dividends tax, it will be exempt from normal income tax.

Dividends tax is categorised as a withholding tax because the tax is withheld from the dividend (income) distribution and paid directly to SARS by the company paying the dividend and/or the withholding agent, such as STANLIB.

Dual-listed companies

Dividends declared by foreign companies listed on the JSE are subject to dividends tax in SA. Foreign withholding tax may also apply to the dividend declarations. Richemont, British American Tobacco and Anheuser-Busch would be examples of such companies.

Example 1

Richemont, a company listed on the SIX Swiss Exchange and the JSE, pays a dividend of R100 to a South African shareholder named Natina. The R100 is subject to Swiss dividends tax at a rate of 35%. This rate is reduced to 15% in terms of the Double Taxation Agreement concluded between SA and Switzerland, whereby 35% is withheld and 20% can be claimed back. Richemont generally provide investors with assistance in this regard. Therefore, Natina only receives R65.

In SA, Natina’s dividend attracts dividends tax at a rate of 20% on the R100. However, as she already suffered an effective 15% Swiss dividend withholding tax, only an additional 5% SA dividends tax will be withheld.

Dividend withholding tax in Switzerland: R35 (35%)

Withholding tax claim: R20 (20%)

Effective Swiss withholding tax: R15 (15%)

South African withholding tax: R5 (5%)

In total Natina will receive a cash dividend of R80 (R65 after Swiss withholding tax + claim of R20 for overpayment of Swiss withholding tax – R5 paid to SARS).

The dual-listed dividend is thus generally subject to tax at the highest effective tax rate between the relevant treaty countries, since a tax credit can be claimed (i.e. no double tax applies). It should be noted that, contrary to Switzerland, many countries only withhold at the reduced treaty rate, subject to receiving the relevant dividend declaration forms from shareholders.

Foreign dividends

There are two ways in which South Africans can invest offshore:

- Via a rand-denominated investment such as a collective investment scheme (CIS); or

- Directly in foreign currency making use of the foreign investment allowance, to invest in a foreign-denominated CIS and/or buying shares in a foreign company by way of an offshore stockbroker account.

In both cases, the investments are in foreign companies that are not listed on the JSE – not dual-listed – and therefore, local dividends tax does not apply. Foreign dividends are, however, subject to normal income tax in the hands of the South African resident taxpayer, subject to certain exemptions or partial exemptions.

As neither STANLIB Multi-Manager, a division of STANLIB Asset Management (Pty) Limited (“STANLIB”) nor its representatives did a full needs analysis in respect of a particular investor, the investor understands that there may be limitations on the appropriateness of any information in this document with regard to the investor’s unique objectives, financial situation and particular needs. The information and content of this document are intended to be for information purposes only and should not be construed as advice. STANLIB does not guarantee the suitability or potential value of any information contained herein.

STANLIB does not expressly or by implication propose that the products or services offered in this document are appropriate to the particular investment objectives or needs of any existing or prospective client. Potential investors are advised to seek independent advice from an authorized financial adviser in this regard. STANLIB Asset Management (Pty) Limited is an authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 37 of 2002 (Licence No. 719).

In order to align the effective tax rate applicable on local and foreign dividends, 56% (25/45) of the foreign dividends arising from a portfolio of shares accruing to a natural person, are treated as exempt. At the highest marginal rate of 45%, this will result in a maximum effective tax rate of 20%; and proportionally less at lower tax rates as illustrated in the table that follows.

A foreign withholding tax may also apply in respect of foreign dividends, which, if applicable, is withheld by the relevant foreign tax authority. Where applicable, a tax credit may be claimed in respect of the foreign tax suffered, limited to the amount of tax payable in SA, even though such dividend may only be taxed at an effective rate of 20%. For example, if a person received only one foreign dividend and no other foreign income during the tax year; and the foreign dividend withholding tax was 12% on the dividend payment, the South African tax on the dividend will be 8% (20% less 12% credit).

Example 2:

Natina opened an account with an offshore stockbroker and bought Apple shares with her foreign investment allowance.

Apple pays a dividend of R100 to Natina. Firstly, withholding tax of 15% is paid to the US tax authority – the rate is reduced from 30% to 15% in terms of the US/South Africa Double Taxation Agreement. Natina therefore receives R85 in her pocket. Apple is not listed on the JSE and Natina does not hold at least 10% of Apple’s shares. Natina pays tax at 45%.

In this scenario, the income tax implications are as follows:

Foreign dividend: R100

Foreign withholding tax: R15

Foreign dividend subject to SA income tax: R100

Minus: exemption (25/45): -R56

Income tax payable: R44 x 45% = R20

Total tax payable by Natina on the Apple dividend: R20 (R15 US withholding tax and *R5 normal tax in SA).

*R20 income tax less R15 rebate/tax credit for foreign withholding tax suffered.

More insights