More savings, less tax – take advantage by contributing more to your retirement fund(s)

Albert Louw

Head of Business Development

Introduction

Remember that all contributions towards retirement funds are tax-deductible in terms of Section 11F of the Income Tax Act. As the tax year-end approaches on 28 February 2023, you can benefit from a tax deduction when filing your tax return for the year of assessment.

The amount of the deduction in a particular year of assessment is limited by Section 11F to the lesser (smaller) of A, B, and C below:

Any contribution over (the smaller of A, B, and C above) that does not qualify as a deduction in the year of assessment, will be carried forward to future years of assessment, subject to the annual limit.

The following examples illustrate the application of these limits

Example 1: Tax saving on current contributions

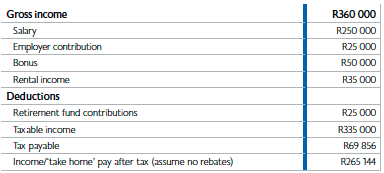

- Mrs Selinda earns an annual salary of R250 000

- Her employer contributed 10% (i.e. R25 000) to a pension fund on her behalf

- She also earned a well-deserved bonus of R50 000

- She earned a rental income of R35 000 (no expenses incurred)

The deduction will be limited to the lesser of the three amounts in bold, which is R99 000. Mrs Selinda only contributed R25 000 and can therefore deduct the full amount of R25 000 for tax purposes.

The following applies under the tax table:

In the example above, for every R1 invested (retirement fund contributions) by Mrs Selinda, SARS will provide tax relief and ‘refund’ her with not less than 30 cents. Her R25 000 annual contribution effectively resulted in a tax saving of R7 558 p.a.

Save more and SARS will provide you with tax relief

Example 2: Tax saving when increasing contributions

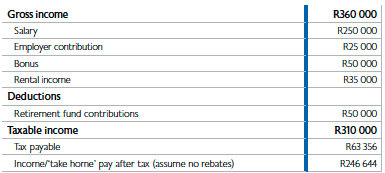

- Mrs Selinda understood the major tax saving and decided to increase her annual retirement contributions from R25 000 to R50 000. After meeting with her financial adviser, her monthly cash flow analysis indicated that she could afford to save an additional R25 000 per year.

- She decided to increase her contribution within her employer’s pension fund by R10 000 (i.e. an additional voluntary contribution) and to contribute the balance of R15 000 annually (before the February tax year-end) towards a retirement annuity from a reputable service provider.

The deduction will be limited to the lesser of the three amounts in bold, which is R99 000. Mrs Selinda contributed R50 000 and can therefore still deduct the full amount of R50 000 for tax purposes.

The following applies under the tax table:

Although Mrs Selinda’s contribution doubled from R25 000 to R50 000 per annum, her take-home pay only dropped by R35 942 per annum (from R282 586 to R246 644). This resulted in overall tax relief of R14 058 per annum.

Dispelling the myth that an additional contribution of say 10% will result in your take-home pay also decreasing 10%

Retirement savings vehicles – pension plans and/or retirement annuities (RAs)

Mrs Selinda had the option to increase her contribution (refer to example 2) within her occupational fund (pension fund) and/or via a retirement annuity (RA). She opted to contribute towards both retirement vehicles. The main reasons for this are:

- Additional diversification – the pension fund follows a specialist investment approach and invests with a single manager. The RA offers more investment choices, allowing her the opportunity to diversify between more than one investment house and investment approach.

- Staggering her retirement needs – when she retires from her pension fund no further contributions can be made. In contrast, you can mature your RA any time after the age of 55. She realises the cost of medical expenses and plans to continue contributing towards her RA once she retires from her occupational fund in order to build up additional savings for post-retirement medical expenses. In this way, making use of an RA to continue saving after retirement for medical expenses.

Retirement annuities: limitations

The law states that it is not possible to withdraw from an RA other than when you have reached 55 years of age; the fund value is less than R15 000; on permanent disability; or if you have been a non-resident for South African tax purposes for a period of three consecutive years on or after 1 March 2021. Hence, if you are thinking of emigrating, you may have to think twice before investing in an RA as you will need to wait three years before you are able to access that money.

Major benefits when contributing more towards retirement

- No tax (income, dividend, or capital gains) is paid on the growth of your retirement savings. Tax is only payable when accessing your savings.

- Retirement contributions are tax-deductible, subject to section 11F of the Income Tax Act. Based on the examples provided, SARS will provide tax relief and ‘refund’ you for contributions made towards your retirement fund savings.

- Flexibility – you can contribute to your existing employer retirement fund and/or via a retirement annuity (RA) or if self-employed, 100% into an RA.

In the unfortunate event of death prior to retirement, RA benefits are not subject to estate duty#, thus saving 20% estate duty tax or 25%, if your estate is greater than or equal to R30 million.

#Any contribution amount to a retirement fund that was not income tax-deductible in the year it was made will be property in the deceased estate. This will be for all deaths occurring on or after 1 January 2016 and for all nondeductible contributions to retirement funds made on or after 1 March 2015. - Discipline – many may disagree that this is an actual advantage, but the fact remains that South Africans are not doing enough to ensure a comfortable retirement. For those less disciplined who may succumb to the temptation of withdrawing from their investments to fund impulsive purchases, a retirement plan (occupational fund and/or RA) is an ideal investment vehicle.

South Africa has several tax initiatives to encourage a savings culture. You should consider taking full advantage of the current legislation if you wish to save more towards retirement. In addition to the annual tax-free amount of R36 000 in an appropriate tax-free savings account, making additional contributions towards retirement savings is a no-brainer.

More insights