In the previous edition of The Educator, we discussed investment vehicles available under the Collective Investment Schemes

Control Act (CISCA). In this edition we briefly introduce wrap funds, also known as “model portfolios”, as an additional investment vehicle for investors to gain exposure to multi-managers.

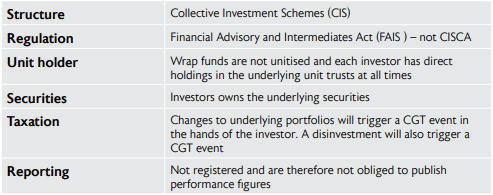

A wrap fund effectively ‘wraps’ a selection of different unit trust funds together. Wrap funds are not classified as fund of funds (FoF’s) as the wrap fund itself is not a collective investment portfolio.

Ownership and management

The investor has direct ownership of the underlying investments via a wrap fund. Wrap funds are not regulated by the Collective Investment Schemes Control Act and do not have a separate legal status. They are controlled by the same legislation pertaining to Linked Investment Services Providers (LISP’s), namely the Stock Exchange Control Act and the Financial Market Control Act.

Who manages wrap funds?

Any portfolio manager registered with the Financial Services Board (FSB) can manage wrap funds. Registered portfolio managers can establish their own wrap funds and act as investment advisor for those funds. Some Linked Product Companies and Asset Management Groups also offer wrap funds.

Who typically uses wrap funds?

Many independent financial advisers manage LISP portfolios on behalf of their clients. Running large numbers of individual portfolios is administratively inefficient and increasingly, advisers are considering consolidation of the individual portfolios into three/four combined (“model”) portfolios according to different risk profiles. For Category 1 Financial Service Providers, these model portfolios may be managed by a multi-manager possessing the experience and processes to construct optimal risk profile portfolios.

Wrap funds can be administered by two types of LISPs

Discretionary – the administration and investment function of the wrap are housed within the LISP

Non-discretionary – the administration is housed within the LISP and the investment function is outsourced

Capital Gains Tax (CGT) – discretionary money

The advent of capital gains tax (CGT) on 1 October 2001 threatened the existence of many wrap funds. Wrap funds are not regulated entities and thus attract capital gains tax each time they sell out of an underlying unit trust and realise a capital gain.