Understanding where asset managers fall in the continuum

Jennifer Henry

Head of Strategic Investments and Manager Research, STANLIB Multi-Manager

An uninformed investor’s predominant method of selecting managers is based on past performance (i.e. managers that have appeared in the top quartile historically); without always understanding the drivers of alpha for the underlying manager. Our research shows that the flaw with this type of selection is that managers who appear in the top quartile in one period do not necessarily persist in this ranking in subsequent periods, meaning that managers who are the top performing managers in one period could go on to become the worst performing managers in the following period.

The importance of understanding that past performance is no guarantee of future performance is the premise on which our manager research function is based. A managers alpha profile is determined by a combination of factors, including; the portfolio manager, the size of the investment team, the investment experience of the team, the organisation of the team and the quality of team discussions, views and debates, the investment philosophy, and finally, the investment process.

While we cannot predict how a manager will perform in future given the uncertainty in the market, we can prepare ourselves with a good understanding of the above dimensions, which then allows us to make great investment decisions based on our expectations.

Within manager research, we place very little weight solely on the actual historical performance of a manager; obviously it is not ignored in its entirety as it provides a litmus test for understanding what type of alpha the manager can deliver given their philosophy and process; for example one would expect that a manager that purports to be style agnostic would deliver a smoother alpha profile over time than a manager that exploits a value style of investing (all else being equal (e.g. both managers are similarly benchmark cognisant or agnostic).

However, in many instances it is other qualitative factors that influence this alpha profile. Therefore it is increasingly important to understand the differing philosophies, styles and processes of managers when making a decision around the combination of these managers into one solution.

Over the coming months, we will provide some insight into a few of the aspects that make managers different, and provide some clarity as to why it is important to understand where managers fit within the continuum that make up our asset management industry.

What makes managers different?

All managers are different but they all have one thing in common in that their primary objective is generating positive alpha over time (i.e. outperforming its benchmark and hence adding value rather than detracting value). Despite this common objective there are a number of aspects that make asset managers different, all of which have implications on their ability to generate alpha over time. We have highlighted just a few of the differentiators that we find important in developing an understanding of these managers:

- Organisation of the manager (i.e. is the manager of a large institutional type manager or a boutique owner-managed business). The organisation of the business has implications for how decisions within the investment team are made

- Size of assets under management, may have consequences for the managers’ ability to extract some premiums that are available

- Value, growth, momentum, valuation, quality – where do managers focus within the market continuum or are more emerging as style agnostic given the limitations of alpha opportunities

- Incentivisation and alignment of interests of the investment team. How invested are managers in their own funds and does this impact investment decisions taken?

- Fundamental bottom-up, top-down or a combination of both in stock analysis and how does this translate into portfolio positions (holdings and sizes, absolute and relative)

- Organisation of the investment team – sector specialists or generalist analysts. Are there implications to this?

- Multi-counsellor (each running distinct portfolios), multiple portfolio managers (all running the same fund), or single manager decision making

We will elaborate on the first three dimensions detailed above in this article.

Organisational structure

The organisation of the manager (i.e. ownership structure) may have significant implications for the investment team in terms of the freedom the team can exercise when making investment decisions. Belonging to a larger holding company or life company may impede the ability of the investment team to express their best ideas for two reasons, firstly satisfying the expectations of external shareholders in terms of delivering shorter term performance while abiding by a long-term investment horison does provide some challenges; and secondly despite having the depth of understanding to express high conviction views, affiliation with a life company may result in the expectation that a manager stay closer to the benchmark as we have seen in a few instances.

As a consequence of these ownership structures and external pressures; more recently we have seen a number of investment teams break away from their parent company to establish smaller, investment focused owner-managed businesses – this would naturally lead one to assume that belonging to a larger business impedes the ability to make investment decisions in the best interests of clients, but is this really the case? What we’ve seen in the analysis of managers is that teams want to focus on making the best investment decisions for clients without “business interference”. It is obvious then that there are pros and cons to both approaches, and this will need to be assessed in the broader context of the managers researched.

Size of assets under management

Size of assets under management may limit the ability of the manager to extract certain alpha premiums. Smaller more nimble managers have the ability to extract the small cap premium where larger managers cannot due to size constraints. Depending on what the market favours over a time period, this may lead to a lost opportunity as a consequence of size. Understanding how the size of a manager limits or expands the opportunity set is important in understanding the type of alpha outcome that the manager can deliver.

If you look at the performance of a universe of equity managers over the period July 2012 to August 2015 the managers that have generated the most alpha over the period have been the boutique asset managers.

Manager styles

One of the most important differentiators for managers is in their manager style. Some managers exploit value type opportunities, while others play more within the momentum side of the market, some purport to be style agnostic enabling the fluidity of moving where the opportunities present themselves. Understanding where managers fit within this continuum is paramount in manager allocation or portfolio construction to achieve a more stable alpha profile with the combination of these managers which is what the multi-manager offering aims to achieve as displayed by Figure 2.

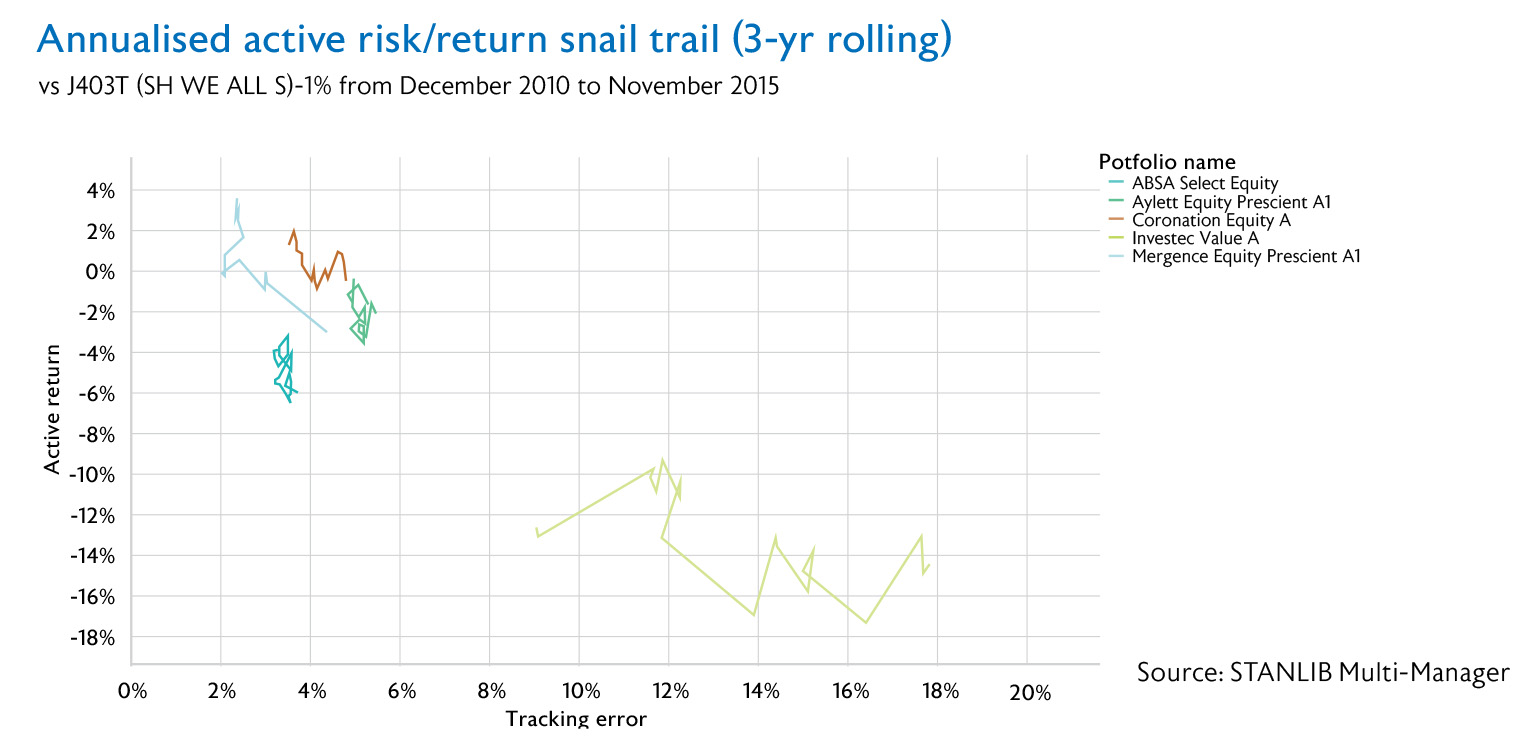

Understanding the philosophy of the manager will allow you to understand how closely the managers will play to the benchmark (i.e. benchmark cognisant or not) and also what type of opportunities the manager will exploit given the style of investing. Figure 3 below reflects the active return against tracking error of a select few managers over the period December 2010 to November 2015 – this highlights how managers’ active return outcomes have evolved over time given the level of benchmark risk taken. We highlight some managers below, ABSA, Aylett, Coronation, Investec Value and Mergence Equity for their equity offering over this period.

Let’s look at Investec Value and Mergence Equity to explain the difference in manager style and how this plays itself out in the portfolio construction. Investec Value for example has a contrarian, deep value benchmark agnostic style as you can see with the tracking error ranging from 10% – 20%. Understanding that this manager is a more deep value, contrarian type manager and what this would mean for diversification purposes when combined with other managers is important. This manager’s style of investing currently has resulted in a portfolio that comprises of resources and cash.

Mergence Equity on the other hand is more benchmark cognisant and style agnostic with a tracking error of around 4% relative to the SWIX, exploiting opportunities within the quality large cap counters. This style agnostic behaviour would allow the manager to move wherever opportunities lie within the market and hence promote a smoother alpha profile going forward. The manager has historically been more skewed to value counters in the past but has now moved to incorporating a more pragmatic value style. One would not be able to understand this evolution of philosophy by focusing on their performance alone.

Understanding these nuances is important when managers are being combined as one would need to ensure that they play to the different dimensions of the market rather than being significantly skewed to just one. Blending these managers together could result in very different outcomes if one does not form an appreciation for how managers’ philosophies translate into portfolio positions. Of equal importance is understanding if managers remain true to their philosophy over time despite the style underperforming.

Conclusion

Managers fall within a broad market continuum. Understanding the underlying philosophy and process of managers and how this translates into decision making is only one aspect; the differences in the manager style, organisation of the investment teams, AUM progression and size, risk management and incentivisation all play an important part in understanding how managers differ as these characteristics all have implications on the drivers of alpha and the performance the manager can deliver over time.