Diversification: Beyond asset classes

Joao Frasco

Chief Investment Officer,

STANLIB Multi-Manager

Diversification comes in many different forms, and at many different levels in the investment process. Investors often forget this, thinking that a fund invested in various shares is well diversified. Thinking about diversification at the security level (e.g. shares) is sometimes simple, but fails to recognise that a single conomy/market/currency/asset class has many idiosyncratic risks that are not diversified when you are invested in just one of them. I will explain idiosyncratic risks in detail later in this article.

Diversification has long been described as the one “free lunch” left when investing, as all other returns require the investor to accept some risk (in which ever form it may take). We like to think of diversification as less of a free lunch, and more of an unrewarded risk that investors should not be taking (idiosyncratic risk is by definition diversifiable, so why would anyone reward you for taking it).

It is sometimes easier to understand how you achieve diversification by considering investing in multiple asset classes e.g. equities, bonds, property and cash. It is also simple to understand that further diversification can be achieved if you invest in many different securities within each of these asset classes e.g. shares and bonds issued by many different companies. Understanding why it is necessary to diversify across different economies and currencies, is a little more difficult.

Understanding idiosyncratic risks

Let’s begin by understanding idiosyncratic risk, as this will provide a great foundation for understanding diversification fully. Let’s consider two “technology” companies (it doesn’t matter which two, and we will therefore not focus on comparing two specific companies). You may think that owning just one of the two companies will give you exposure to technology companies, but you would only be partially (and potentially very marginally) right. Both companies may have exposure to global trends in technology, but there is no guarantee of this.

The companies could operate in different countries (subject to different laws and regulations), have revenues from different geographies, industries and clients. They could provide completely different products and services (some of which may be well established product lines with little or no future prospects for growth, while others which may have very little current revenue prospectus but massive future opportunities). The companies are run by different people (management and staff), who all have different backgrounds and experiences, which will inform their business practices and strategies. The list of differences goes on and on.

Over the short term, macro events could force these companies’ shares to perform in a similar way, leading investors to focus too heavily on the lack of diversification provided, but this is one of the most misunderstood aspects of what diversification purports to offer (investment horison is critical). Over the long-term, no two companies will share the same fate. Apple almost shut down in the mid to late nineties, and is now the largest market cap share in the world. Microsoft didn’t exist fifty years ago, and their software sits on most home and business personal computers today. Facebook and Google hardly existed a decade or two ago, and are some of the biggest technology companies in the world. Extending the investment horison to months and years will quickly highlight the benefits of diversification, not only between two companies/shares, but also between two asset classes/markets.

To summarise, every variable and decision will make two companies different, creating idiosyncratic risk. While combining two such companies will not remove the risk of the macro factors that will affect both companies (e.g. currency depreciation), it will diversify those idiosyncratic risks.

This is all of course very well understood by all investors (professionals, amateurs and the lay person alike), so everyone ensures that portfolios are well diversified across all of these variables, the most important of which are asset classes (including geographies / markets / currencies), and across securities within asset classes (for example, shares and bonds from different companies / issuers). To the extent that you want maximum diversification, we could all invest in the market portfolios (the portfolio of all investible assets, which is very different from just investing passively in a single index that comes with its own idiosyncratic risks).

Single manager funds introduce further idiosyncratic risks

What are the alternatives?

You could, as an investor, do this yourself i.e. just invest in a couple of funds to diversify single manager risk, but you shouldn’t be doing this on other people’s behalf without doing the required due diligence work

on all the single managers you choose to invest with. This is one of the primary functions performed by a multi-manager i.e. research the universe of available managers to understand their philosophies and processes with the objective of forming a view on which managers are likely to outperform over the medium to long term, and which managers to avoid.

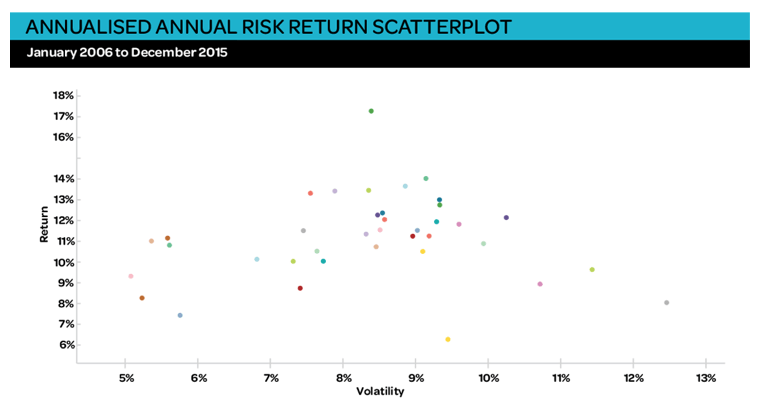

You can perform the exercise above across other asset classes and across other regions in the world, and you will find very similar results, which is why multi-management is growing so quickly around the world. As markets get more complex, more asset managers enter the market to facilitate understanding and extract value for clients. They in turn bring their own complexity, which multi-managers and consultants enter the market to address. Asset managers make markets more efficient through price discovery (and information discovery), and multi-managers make the asset management industry more efficient by allocating capital to the best managers and taking it away from those that destroy value for clients.