While our long-term real return assumptions are derived assuming that markets are in equilibrium, we do not believe that this is the case all the time. We therefore take tactical views on the relative performance of each asset class over a three to 12- month period, specifically ignoring shorter-term noise and not relying on long-term expectations. Having identified a specific factor or catalyst for the relative out- or under-performance of an asset class, we then rate it on a scale of underweight/neutral or overweight and position our portfolios accordingly.

* Floating rate instruments of maturity longer than one year.

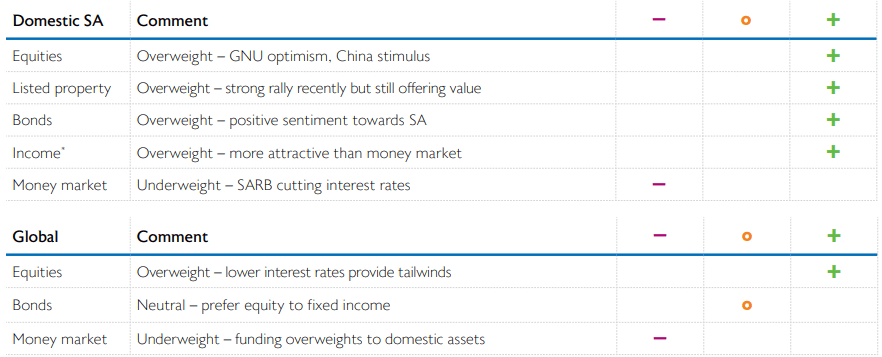

** Views expressed for each asset class are subjective and are for the asset class as a whole. All views are as at 30 September 2024.

Domestic asset classes

Equities

- The FTSE/JSE Capped SWIX Index continued to rally in Q3 as investors remained optimistic about the prospects of the GNU. In addition, the stimulus package from the Chinese government and the beginning of the interest rate cutting cycle by both the US Fed and the SARB provided further support for SA equities. On the back of this, the local bourse rallied 9.6% in Q3 and is up 25.4% over the past year.

- • We increased our overweight position to SA equities early in Q3 to take advantage of cheap valuations in domestic assets and to benefit from the GNU exuberance. Despite the recent rally in the past two quarters, SA equities are still cheap. They trade on a 10x forward PE, 1.5x Price-to-Book and offer a decent yield of 3.7%.

Listed property

- Locally listed property was one of the biggest beneficiaries of the GNU-induced rally in domestic assets, gaining 19.1% for the quarter to take its one year return to an impressive 51.0%. The start of the interest rate cutting cycle and improving fundamentals also helped.

- Despite the recent rally, this once loved asset class is up only 5.1% over the past five years, carrying the scars of the collapse of the Resilient group of companies in 2018. The sharp moves in property are testimony to the low valuations in the sector – still trading at a 20% discount to NAV.

- We remain overweight domestic property as we believe it is still undervalued with positive tailwinds.

Bonds

- The FTSE/JSE All Bond Index (ALBI) returned 10.5% for the quarter, fuelled by the rally in the 12+ area of the curve, which gained 14.2%. Over the past year, the ALBI is up an impressive 26.1%.

- We have been overweight domestic bonds for some time now as we believed investors are too punitive on the pricing of SA sensitive assets.

- Given the rally in the past few months, we took some profits from the position but remain overweight. Bond yields at the long end of the curve are still running above 10% and recent inflation prints (4.4% in August) point towards falling inflation. Potential real returns from the asset class remain high.

Income

- Income returned 3.7% in Q3, significantly lagging bonds but still ahead of domestic cash. In the past year, income has gained 12.5%.

- Income typically enjoys a 50 basis point yield advantage over cash yields but more recently, its yield has dropped and is currently 10 basis points lower than cash. Ordinarily, we would cut back our exposure but given our expectations of interest rates cuts in the next 12 months, we think it can still outperform cash.

Money market

- Most central banks, including the SARB, are on a rate cutting cycle. Investors expect the local central bank to cut interest rates by a further 75 basis points between now and 2026. We also share these expectations and as a result, remain underweight cash.

Global asset classes

Equities

- The MSCI AC World Index rallied 6.7% in US dollar terms in Q3 to take its one year return to 32.3%. US equities continued to contribute the most to returns but China returned 23.8% in September, which also added to the quarter’s return.

- The US Fed joined other central banks in September, cutting interest rates by a larger than anticipated 50 basis points. Investors welcomed this as a sign that it can indeed engineer a soft landing for the US economy.

- We added to our overweight position in global equities during September, as we think the beginning of the interest rate cutting cycle will provide further tailwinds for equities. Valuations are a bit stretched but not overly demanding.

Bonds

- The yield on the benchmark 10-year US Treasury Note dropped to 3.7% from 4.3% at the end of June, to snap a two-quarter streak of rising yields. The Bloomberg Barclays Global Aggregate Index gained 7% in US dollar terms in Q3. Over the past year, global bonds have gained 12.2%.

- We closed our overweight position to global bonds in Q3. With the rate cutting cycle commencing, we prefer equity to fixed income assets.

Money market

- We are underweight global cash as we prefer domestic assets to offshore assets.