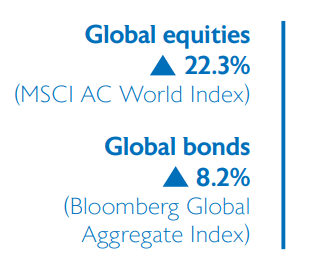

Global equity markets ended 2025 on a strong note, having notched up double-digit returns in a turbulent year that was dominated by tariff wars, AI mania and simmering geopolitical tensions.

President Trump’s hardline tariff agenda became one of the most consequential stories of the year and few predicted the end results or how wild the ride would get. The plan was to put ‘America First’ and aimed at reviving a declining manufacturing base. The increased tariffs lifted the average rate to nearly 17% from less than 3% at the end of 2024, according to Yale University’s Budget Lab, and are now generating revenue of roughly $30 billion a month for the US Treasury. They brought world leaders scrambling to Washington seeking trade deals for lower rates, often in return for pledges of billions of dollars in US investments.

Trade deals were reached with a host of major trading partners but notably, a final agreement with China — the world’s second largest economy — remains on the incomplete list despite multiple rounds of meetings and a face-to-face meeting between President Trump and Xi Jinping. China used the leverage it has gained in rare earth minerals — crucial inputs into the West’s security scaffolding — to push back against pressure from the US to increase more tariffs. US Treasury Secretary Scott Bessent described China’s actions as “pointing a bazooka at the supply chains of the Western world.”

The Fed cut interest rates three times in 2025. At its last meeting in December, they lowered the benchmark interest rate to a range of between 3.5% to 3.75%, as officials agreed that a slowdown in monthly employment and rising unemployment warranted slightly less restrictive monetary policy. But new projections show only one rate cut is expected this year and any further cuts are likely to be kept on hold for now until new data shows that either inflation is falling or unemployment is rising more than anticipated.

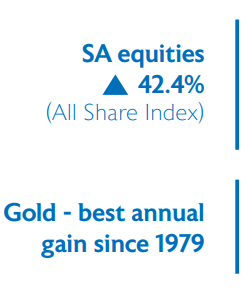

The FTSE/JSE All Share Index gained 42% in 2025, driven largely by an extraordinary run in the mining sector – resources were up 126%, benefitting from a commodity price windfall. Gold, silver and platinum jumped to all-time highs to extend a historic end-of-year rally for precious metals.

Safe-haven gold gained 65% last year, driven by multiple factors, including geopolitical and economic uncertainties, expectations of US rate cuts, strong central bank buying, the ‘de-dollarisation’ trend and robust exchange-traded fund inflows. There were massive returns from gold companies — Gold Fields (up 200%), AngloGold (up 242%), Harmony (up 124%), Sibanye (up 313%) and Implats (up 204%).

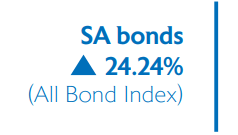

The JSE All Bond Index gained an impressive 24.2% in 2025. The bond rally has been supported by the SARB cutting the benchmark repo rate by 1% last year. This after inflation eased to a five-year low and geopolitical noise seems to have quietened down for now. The 10-year government bond yield fell below 9% for the first time in more than seven years.

Money market assets gained a respectable 7.5%.