Risk profiling – combining multiple factors as part of goals-based financial planning

Albert Louw

Head of Business Development

Executive summary

- Risk profiling is principle-based and little guidance is provided by the regulator on how an adviser should determine the risk profile of a client

- However, as part of goals-based financial planning, risk profiling has evolved. Many financial advisers are now able to use advanced software tools that allow them to perform more holistic financial planning

- Financial advisers are able to combine multiple factors – risk required, risk capacity and risk attitude – to determine a more accurate risk profile for clients

- It is crucial for advisers to ensure that clients are educated and understand their true risk profiles.

Background

The Financial Services Conduct Authority (FSCA) recognises the importance of risk profiling and as such, it is included in their regulation dealing with the suitability of financial advice. However, the regulation on risk profiling is principle-based and provides little guidance on how an adviser should determine the risk profile of a client. This has resulted in many different risk- profiling questionnaires, each with its own questions, weightings and multiple approaches to form the risk profile of a client.

In this article we briefly highlight some of the flaws that exist with risk profiling. We discuss how advisers can evolve approaches by combining risk components to lay the foundation for goals-based financial planning.

Traditional risk profiling approach – flaws with one-dimensional measurement

Many advisers have advanced from single-dimension measurement of risk profiles by using advanced planning software. However, there are still service providers with an advice process and compliance that “allows” planners to get their clients to complete a risk profile questionnaire that focuses on risk tolerance.

This process implies that the risk tolerance of a client is equivalent to his or her risk profile. This is misleading. The outcome – conservative, moderate or aggressive – is then used to select investments such as a conservative, moderate or aggressive investment portfolio.

This is a process whereby the adviser is able to “tick all the boxes” and is deemed to be compliant. However, the outcome may not serve the best interests of the client. Although most of these risk categories – conservative, moderate or aggressive – have some general, subjective descriptions, they are, by definition, entirely open to interpretation unless some quantifiable objective is added.

The traditional approach to risk profiling has little to do with meeting the objectives, or goals, of a client. If an adviser invests a client’s money according to his/her aggressive risk profile for example, neither the adviser nor the client would know whether the investment will meet the needs and/or objectives of the client, as required in terms of the Code of Conduct. Section 8(1) (c), states that an adviser must seek appropriate product(s) in accordance with the client’s risk profile AND financial needs.

What is the most appropriate way to determine the true risk profile of a client?

The request for a client to complete a risk profiling questionnaire marks the start of a conversation about risk. Only through a thorough and carefully structured conversation as part of a systematic approach to investment advice, can advisers understand the true investment risk profile of a client.

This is the reason why we need to provide context to the meaning of the risk profiling that we envisage in terms of the Code of Conduct. A multi-dimensional process combines many factors – subjective and objective – to create a true risk profile or rather, an overall assessment of the most appropriate level of risk for a client.

Risk profiling in practise

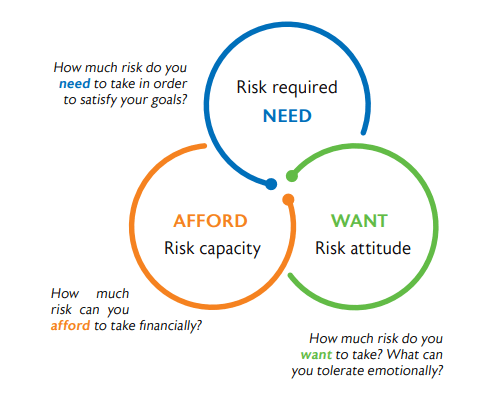

The risk profile of a client is built upon three primary considerations – the risk they would be required to take to generate sufficient return, their capacity for risk and their attitude towards risk.

Most reputable financial planners, locally and abroad, start with an assessment to assess a client’s attitude to risk. The rationale behind this is that although each investor is unique, it is possible to categorise clients’ attitudes to risk using proven psychometric profiling techniques. Such an assessment measures psychological factors including intelligence, aptitude and personality traits. Aspects such as tolerance for ambiguity, desire for profit and investment experience are good indicators of a tolerance for risk and how a client may feel about taking risk with an investment.

The question is whether it is the correct approach to determine the risk profile of a client with analysing subjective factors, before educating that client. Is it possible to test the risk tolerance of an investor, without educating him about the behaviour of investments? By this we mean risk aversion (the risk of losing capital), timing the market, greed, fear, etc. For goals-based financial planning it is important to educate the client – so that he understands the advice – before it is possible to have a meaningful discussion of the lifestyle goals that must be transformed into financial goals and investment strategies.

Step 1 – risk required

The first step should be to determine the financial needs of a client. This requires focused questioning to uncover the financial position and objectives/goals of a client. The aim of this discussion is to understand the objectives of the client – whether it be income, capital growth or a combination thereof.

Determining the term and risk required are objective tests. Only once a client is educated about various inflation-beating investments strategies, can one move onto risk capacity and finally risk tolerance. Thus term and inflation should be approached in an objective manner.

Example

What should the financial planner do? If they have highlighted the inflation risk over the long term, together with the risk of longevity and explained the fundamental investment principles as captured with goals-based financial planning, then the adviser is free to enter into the contractual relationship with the client and proceed on that basis.

It is therefore not the outcome – namely the portfolio that the adviser has selected – that will determine whether they have dispensed the correct or incorrect advice, but the process they followed in order to get there. Risk required is thus the risk associated with the return required to achieve a client’s goals, taking term and inflation into consideration.

Step 2 – risk capacity

The next step is to assess how much risk the client can afford to take financially? The examples below illustrate this concept.

Example A

Based on the information gathered, John has a high-risk capacity. Given his overall financial position, he can take on higher risk in his portfolio, meaning more growth assets.

Example B

Given his overall financial position, Peter has a low-risk capacity. Peter cannot take on higher risk in his portfolio, meaning fewer growth assets.

It is for this reason that we regard the logical order of any investment to be firstly the risk required. This would be followed by risk capacity and finally adjusted by risk tolerance. The risk tolerance – discussed below – is likely to be the final factor in finalising and cementing the contractual relationship – a very logical order. Such order makes sense since the client and financial planner finalised their discussion with a contractual undertaking that may eventually deviate from the overriding requirement, namely risk required or objectives. This is perfectly in line with Section 8 of the Code of Conduct.

Step 3 – risk tolerance

Risk tolerance is clearly a subjective test and should never form the starting point of any attempt to establish the risk profile of a client. It is a psychological parameter. Risk tolerance could be a balancing factor and the final step to the contractual relationship with a client, as per the Code of Conduct.

Simply put, risk tolerance is how a client feels about taking risk. Where the client strikes the emotional balance between seeking a favourable outcome versus risking an unfavourable outcome.

At this stage there are many options available should a client not accept the investment solution proposed by a financial planner. He may select a higher risk portfolio primarily made up of growth assets – equities and property – and want the highest possible return on his capital, not suffering from regret to any extent, despite not having the risk capacity for this portfolio. This is how we balance risk tolerance with risk capacity.

The above is nothing more than investment and financial planning strategies working hand in hand to ensure value-added financial planning.

Clients need to be empowered to make informed decisions

From a goals-based financial planning point of view, a client should be at the centre of every disclosure. In order to enable a client to make an informed decision, all relevant and material disclosures about investment risk and the risk taken need to be provided. Hence client education on investment planning and risks are crucial.

Explaining various risks to clients helps them to gain a better understanding of the risks of investing. This includes shortfall risk – failing to meet goals – or, in its simplest form, that the value of his investments may decline over a given period, as well as explaining that the investment is exposed to downside risk. These concepts need to be quantified in simple and understandable terms.

Financial planners also have a duty to provide advice with due skill, care and diligence. Therefore, they need to caution a client if risks taken or agreed on, are not suitable considering all the information collated from the client and the subsequent outcome of the overall assessment.

Lastly, client information and the risk profiling analysis need to be properly documented in the advice process. The record of advice furnished to the client must reflect the basis on which the advice was given. Ultimately, the final decision rests with the client and it is imperative that any deviations from the recommendations made by the financial planner should be kept on record.