When investing offshore do not overlook the importance of estate planning

Albert Louw

Head of Business Development

EXECUTIVE SUMMARY

- When investing offshore, many investors believe that since you pay estate duty in South Africa on worldwide assets, no additional death taxes are payable outside of South Africa.

- That is not necessarily the case, as we attempt to demonstrate in this article. Should you be liable for foreign inheritance/estate tax, an estate duty treaty or domestic legislation may provide some relief, but additional taxation may potentially still apply.

- The treatment of estate duty and the law of succession need to be considered appropriately. In some cases, estate taxes may apply, but not law of succession, or vice versa.

- It is also important to determine whether you need to consider an offshore will for example in counties with forced heirship/law of succession..

Background

South Africa is a small economy when seen in a global context, with only 0.5% of world GDP according to a Goldman Sachs report. It should therefore not come as a surprise that increasingly, more South Africans have decided to further diversify their investments by investing in global markets. However, owning foreign assets gives rise to the need for good estate planning.

WHY?

Many of us are familiar with income and capital gains tax (CGT) when investing offshore, but death taxes and the law regarding succession also need to be considered. Investment decisions without proper estate planning could have major ramifications.

Estate duty on offshore assets

If you are ordinarily resident in South Africa, your worldwide estate is subject to the South African estate duty system and as such, estate duty applies. This is because the South African tax system is based on residency and not the source of funds, meaning that it is not only the assets based in South Africa that are included for estate duty purposes.

By way of an explanation, if you have a property in Mauritius, it will be taken into account when calculating your estate duty. Estate duty is applicable to the worldwide dutiable property of the deceased’s estate.

The current legislated estate duty rate is 20% on the value of the estate up to R30 million and 25% on estates greater than R30 million i.e. 20% on first R30 million and 25% on the value above R30 million.

Additional estate/inheritance taxes in the foreign country

We know that South African residents pays tax on worldwide assets/income. However, it is also important to know that an investor investing offshore may also be liable for estate duty offshore, typically referred to as inheritance tax and/or estate taxes. In many countries no estate taxes are payable if you are not a resident or a citizen of the country where the assets

are situated.

However, in counties such as the US and the UK, if you do not have residency/citizenship in the US or residency/domicilum in the UK, you may still be liable for estate/inheritance taxes on assets that you have in these countries (an example would be immovable property or shares in US or in UK corporations).

Potential ‘tests’ that may be applies to establish whether you will be liable for estate duty offshore include jurisdiction, type of asset, legal vehicle, value of investment, tax residence and domicile or citizenship of the investor.

Jurisdiction

The first ‘test’ is jurisdiction. An equivalent type of tax to local estate duty is levied in many other jurisdictions and is dependent upon the ‘situs’of the assets. The word ‘situs’ simply refers to the source or location of the asset, for example the US or the UK. Situs is the Latin word for ‘position’ or ‘site’.

The situs of an asset is generally the place where the asset is deemed to be located for legal purposes. In the US, we refer to ‘estate taxes’, while in the UK we refer to ‘inheritance tax’. It is likely that other jurisdictions may also impose an equivalent type of tax on your estate in the event of death.

Type of asset and investment vehicle

The type of asset and/or investment vehicle used is an important test. For example, the situs of immovable property is the place or country where the property is situated, or in the case of equities, generally where the share register is maintained.

If you have your own broker account – i.e. you invest directly into foreign shares – you may be liable for additional estate taxes in jurisdictions such as the UK or the US. If, for example, you have a stockbroking account in Jersey – the location of the stock broking account is irrelevant – and at death, you own Apple shares, which are registered in the US, it means that the Apple shares qualify as a US situs asset in the event of your death and may be subject to estate tax in the US.

However, there are various ways to gain exposure to offshore assets that may mitigate additional estate taxes as a result of the situs of an asset. This could be achieved by investing in funds or through vehicles that may not be considered as situated in a country where such a tax applies to non-residents of that country – even if the South African investor holds the underlying situs assets.

Potential solutions may include using:

- Foreign collective investment schemes (CISs);

- Open ended investment companies (OEICs);

- Exchange Traded Funds (ETFs);

If a South African investor acquires units in a suitable foreign collective investment scheme/unit trust domiciled outside the jurisdiction in question – or within such jurisdiction but is regarded as an ‘excluded asset’ – inheritance or estate taxes may not arise on the death of the unit holder even though the underlying assets in the fund may have a high exposure to specific onshore stocks. This is because the unit holder’s rights are to the units held in the fund and not in the underlying fund assets.

- Insurance wrappers such as endowments.

Investors may hold an investment portfolio via a life wrapper, e.g. an offshore endowment, in which case, the assets held within the wrapper may be disregarded as a situated/situs asset.

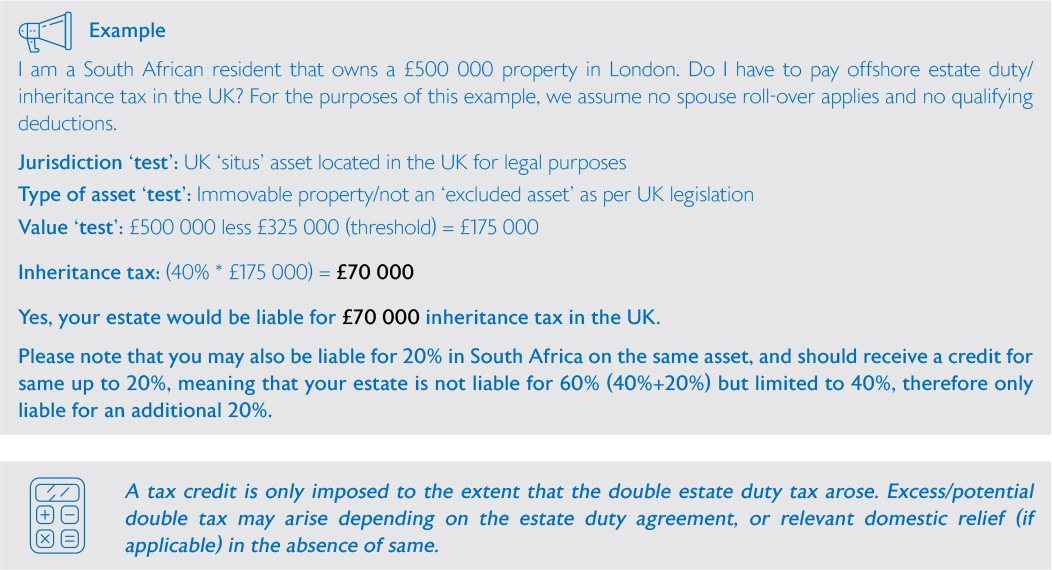

Value

Typically, there are thresholds upon which you as a non-resident and non-domiciled individual will be liable for estate taxes offshore. In the UK inheritance tax is currently levied at a standard rate of 40% if the value of your assets is more than £325,000. In the US estate duty is levied from 18% to a maximum of 40% with a $60 000 threshold applicable to persons who are not a citizen or resident in the US.

Estate tax treaties/double taxation conventions

South Africa has estate tax treaties with some countries1 to eliminate potential double taxation in relation to estate duty.

These treaties aim to determine which jurisdiction has the primary taxing right and which has to exempt or provide a credit. The country where an asset – for example immovable property – is situated, generally has the first right to tax. In the absence of an estate duty agreement/estate tax treaty, your tax adviser or an executor would need to consider other forms of domestic relief, if applicable. Such relief may for example, include providing for a deduction of any liability for estate duty in another country against the dutiable estate rather than providing a credit. Double taxation may therefore still arise.

Both the US and the UK have entered into an estate duty agreement with South Africa. Since South Africa taxes the value of the dutiable estate at 20%, local tax authorities will only grant a tax credit to the extent that double tax has been imposed and up to the amount of estate duty payable in South Africa. Should another jurisdiction impose a tax in excess of that, the excess tax remains applicable in the respective foreign jurisdiction, for example potentially in the UK.

Forced heirship rule/law of succession

Forced heirship is a set of rules that restrict the testator’s freedom to distribute his/her estate, or a portion thereof, in order to protect certain heirs, such as a spouse, children and/or other close relatives. In several countries where this system applies, a portion of the estate is subject to the laws of forced heirship and distinguishes between immovable and movable assets being applicable or not applicable to same, while the balance is left to the testator’s discretion.

A South African will works well if you have investments/assets in countries that also enjoy the freedom of testation. However, if you own assets in a country where forced heirship laws apply, you may contemplate drafting a separate will for your offshore assets in that jurisdiction.

It is important to bear in mind that each country has its own set of laws regarding the drafting of wills. Some countries will recognise a will drafted in South Africa, whereas the legislation of others may deem a South African-drafted will to be invalid. You therefore need to consider all options when you have assets offshore and forced heirship rules are in place.

Albert Louw CFP®

STANLIB Multi-Manager: Head of Business Development

South Africa has entered into Estate Duty agreements, with the following countries: the United States of America, the United Kingdom, Zimbabwe, Botswana, Lesotho and Swaziland