“A regular company makes profit and pays taxes on its entire profit. There-after, the decision is made as to how to

allocate after-tax profits between dividends and reinvestment. A REIT simply distributes all of its profits and gets to skip

the taxation”

In this issue of Educator we briefly discuss the rationale for the REIT structure and how the legislation impacts you as a shareholder in listed property stocks and/or as an investor in a property Collective Investment Scheme (CIS).

Allow both PLSs and PUTs to convert to a REIT

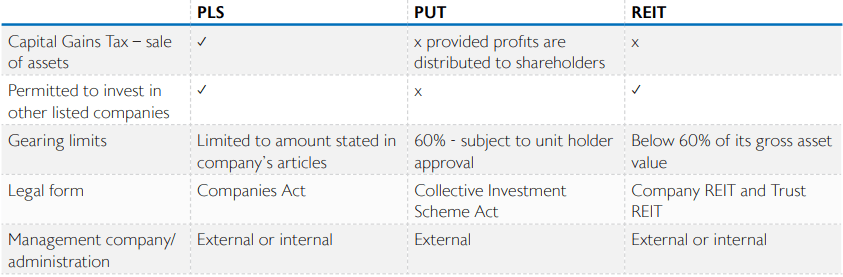

Prior to SA REIT legislation, there were historically two forms of listed property investment entities, namely Property Loan Stock (PLS) and Property Unit Trusts (PUTs). The complexity around PLSs and PUTs was difficult for investors to understand and caused confusion as to how income distribution was taxed.

The REIT regulations incorporate listed property stocks (PLS and PUTs) under a single umbrella and provide clarity on which investors are taxed.

Taxation – how it impacts you as a natural person

SA REITs provide a simple and clear tax structure.

*Take note: Where the recipient is a non-resident investor, the dividend will remain exempt from income tax. Effective 1 January 2014, a 15% withholding tax is imposed on their distributions or the double tax agreement rate where applicable.

Capital Gains Tax

Shareholders/unit holders continue to be exempt from Capital Gains Tax (CGT) until such time as they sell out of their REIT investment/CIS.

Summary

Converting PLSs and PUTs to REITs allows for better uniformity, transparency, tax dispensation and investor protection

REITs are globally recognised and in line with international standards

Under the REIT regime, the South African listed property market benefits from increased interest from foreign investments on the back of more transparent and single-tax rules

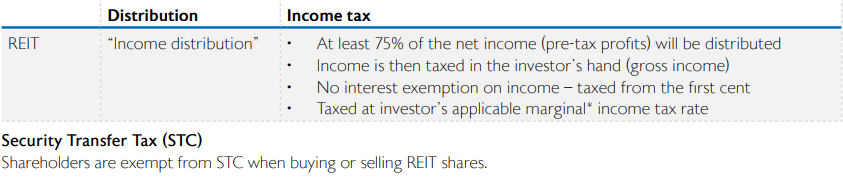

Investors can be certain that 75% of the net income is distributed – flow through of net property income

Income distribution is taxed at the investor’s marginal tax rate